Fixed Income Budgeting: Financial Tips for Retired Older Women

Retirement can be a wonderful time to enjoy life, but it also requires careful financial planning, especially when living on a fixed income. For retired women, ensuring financial stability is crucial. With many relying on pensions, social security, and savings, managing a fixed income becomes essential to maintaining a comfortable lifestyle. So, how can retired women navigate their finances without stressing out? This article explores practical budgeting tips and financial strategies that can help older women thrive during retirement.

1. Understanding Fixed Income and Its Challenges

A fixed income typically refers to a steady source of income that doesn’t fluctuate, such as Social Security, pensions, or savings withdrawals. While it provides some financial security, it also means that spending must be carefully managed. According to the National Institute on Retirement Security, nearly 70% of women over 65 depend on Social Security for at least half of their income. This makes budgeting even more crucial.

Challenges of a Fixed Income:

Rising Healthcare Costs: As women age, healthcare becomes a major expense. On average, retirees spend 15-20% of their income on healthcare.

Inflation: The cost of living tends to rise over time, eroding purchasing power. Without increasing income, retired individuals may find themselves unable to keep up with rising costs.

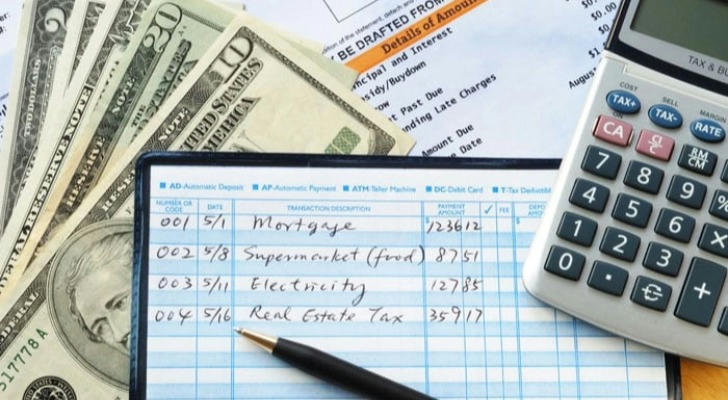

2. Create a Realistic Budget

The first step in managing a fixed income is developing a clear, realistic budget. Knowing exactly how much money is coming in and going out each month is crucial for financial success.

Steps to create a budget:

Track Monthly Income: Make a list of all sources of fixed income, including Social Security, pension, or annuity payments.

List Essential Expenses: Identify necessary expenses, such as housing, utilities, transportation, and food. These costs should always be prioritized.

Include Discretionary Spending: Budget for personal enjoyment, like hobbies, entertainment, or dining out. While it’s important to be frugal, enjoying retirement is just as important.

Factor in Savings: Even on a fixed income, setting aside some money for emergencies or unexpected expenses is vital.

3. Prioritize Healthcare Costs

For retired women, healthcare expenses can become the largest part of the budget. According to Fidelity’s Retirement Savings Assessment, a 65-year-old couple retiring today can expect to spend an average of $300,000 on healthcare throughout retirement. Managing healthcare costs wisely is essential to stretching a fixed income.

Tips to manage healthcare costs:

Medicare: If eligible, Medicare can cover many healthcare expenses. However, it doesn’t cover everything. Consider purchasing additional coverage (Medigap) to fill in gaps.

Preventative Care: Regular check-ups and preventative care can reduce long-term healthcare expenses. Investing in wellness now may save big in the future.

Compare Healthcare Plans: Shop around for the best rates on insurance plans and prescription medications. Many companies offer discounts for retirees.

4. Save Where Possible

Living on a fixed income doesn’t mean there’s no room for savings. Even small amounts can add up over time and provide a safety net for unexpected expenses.

Ways to save on a fixed income:

Cut Back on Unnecessary Expenses: Identify non-essential spending that can be reduced or eliminated. Small changes like canceling unused subscriptions or reducing energy usage can help.

Downsize: Consider downsizing to a smaller home or apartment. This can reduce mortgage or rent payments, as well as property taxes and utility bills.

Use Senior Discounts: Many retailers and services offer senior discounts. Take advantage of these savings whenever possible.

5. Investing for the Future: Low-Risk Options

While it’s tempting to keep savings in a savings account, inflation can reduce the purchasing power of money sitting idle. Retired women may benefit from investing in low-risk financial products that can provide a steady return over time.

Low-risk investment options:

Bonds: Government or corporate bonds provide a reliable income stream without high risk.

Dividend Stocks: For those with a bit more risk tolerance, investing in dividend-paying stocks can provide regular income.

Annuities: Annuities can guarantee a steady income for life, though it’s essential to understand the terms and fees before committing.

6. Plan for Emergencies

Retirement may offer peace of mind, but unexpected situations can still arise, such as medical emergencies or urgent home repairs. Having an emergency fund is vital, even on a fixed income.

Building an emergency fund:

Set Aside a Percentage: Consider setting aside 3-6 months’ worth of expenses in an easily accessible account.

Avoid Using Credit: If possible, avoid relying on credit cards to cover emergencies. High-interest rates can quickly accumulate debt.

Look for Assistance Programs: There are numerous local, state, and federal programs that can assist with healthcare, housing, and other emergencies. Research these options regularly to stay informed.

Conclusion: Empowerment Through Financial Planning

Living on a fixed income can be challenging, but with the right budgeting and financial strategies, retired women can live comfortably while maintaining their independence. By tracking expenses, managing healthcare costs, prioritizing savings, and investing wisely, it is possible to make the most of retirement. Financial planning is about more than just surviving; it’s about thriving in your golden years.